What Is the Best Gold Bar to Buy?

Gold has mesmerized people for centuries with its sparkling beauty and enduring value. It is like an eternal treasure hidden beneath the surface of the

Gold has mesmerized people for centuries with its sparkling beauty and enduring value. It is like an eternal treasure hidden beneath the surface of the

Investing in a diverse range of assets is essential to safeguard oneself against the devaluation of any single asset. Diversification is a risk management strategy

Successfully navigating crypto investments’ volatile and intricate realm requires a prudent approach and in-depth market knowledge. To make wise crypto investments, it is crucial to

Price action represents the fluctuation of a security’s price over time, a foundational concept in trading. It emphasizes analyzing price chart patterns to guide trading

Fixed-indexed annuities (FIAs) are popular among investors seeking a balance between market participation and downside protection. These annuities offer growth potential based on an underlying

It is crucial to emphasize the importance of due diligence when investing in off-plan projects in Dubai. Whether you are investing in flats in residential complexes

A gold dealer is a business or individual that buys or sells physical gold. However, not all gold dealers are created equal. While some specialize

Cryptocurrency, a digital or virtual currency utilizing cryptography for security, has grown exponentially since its introduction, disrupting multiple industries, including gaming. The gaming industry, a

Introduction The distinction between conventional fiat currency and digital assets has turned progressively salient in the contemporary, swiftly advancing monetary domain. This composition endeavors to

Forex trading can be lucrative for anyone willing to put in the effort to learn the basics. While it can initially seem overwhelming, with some

Cryptocurrency, which is a form of virtual currency utilizing secure cryptography techniques and independent of government or financial institutions, is becoming increasingly popular in the

Trading foreign currency has become a popular side hustle to generate part-time income. The global market for currency exchange offers lucrative investment potential, but prospective

Many companies have considered adopting ESG strategies because they believe the world is changing. Besides, some investors feel obligated to support companies with good environmental

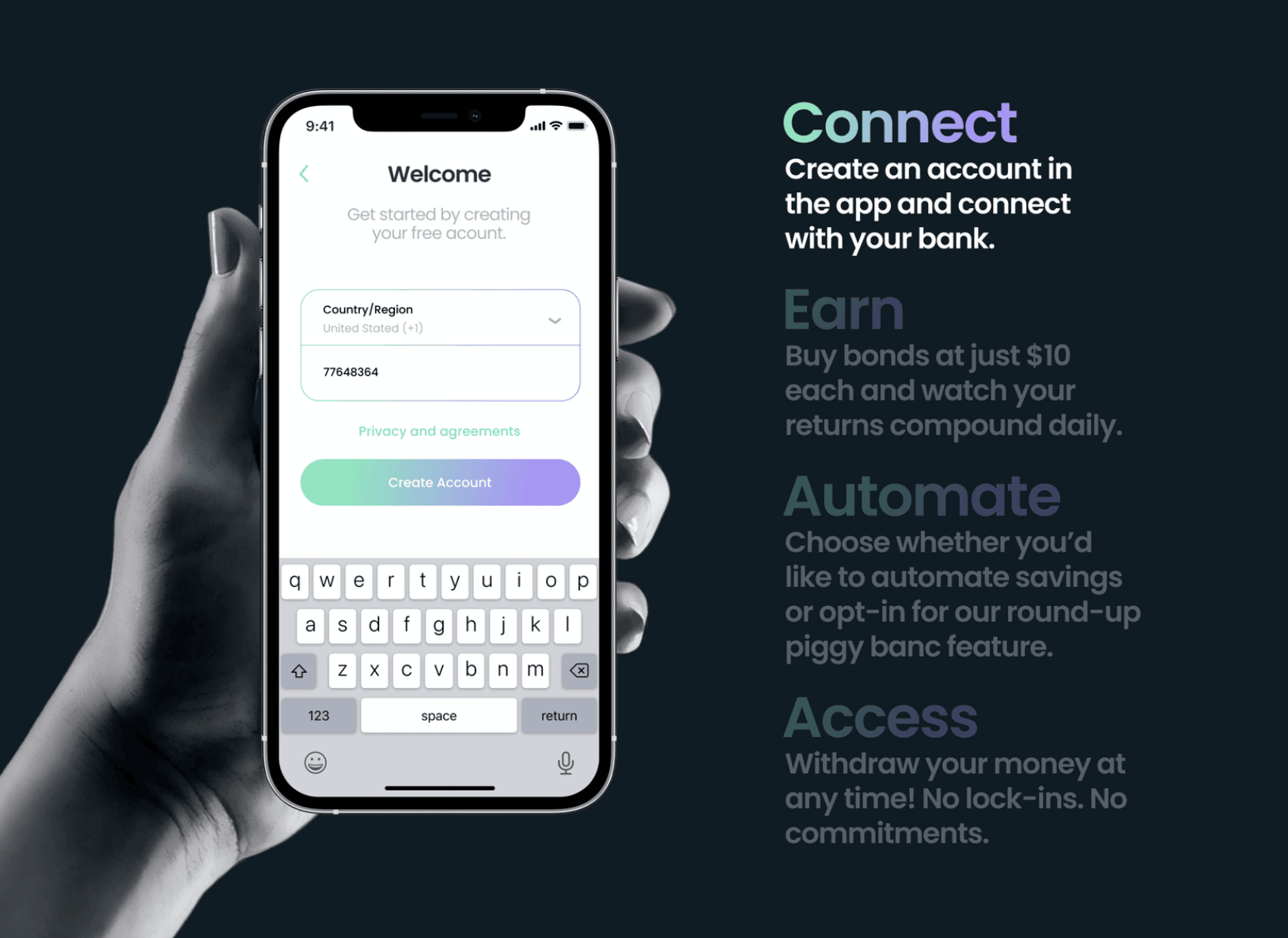

Compound Banc is a financial technology (Fintech) company that provides access to institutional-quality real estate investments and products to retail investors. They offer low-cost, tax-advantaged

50% OFF No Code Needed 2023 Trade and Travel 2.0 Early Bird Special! Save $5,000 off Teri ijeoma’s New Trade and Travel 2.0 course. Get