Cracking the Code: Understanding Credit Reports for Pre-retirees

Gain insight into decoding credit reports to make informed financial decisions as a pre-retiree. Understand how credit reports impact your retirement planning.

Gain insight into decoding credit reports to make informed financial decisions as a pre-retiree. Understand how credit reports impact your retirement planning.

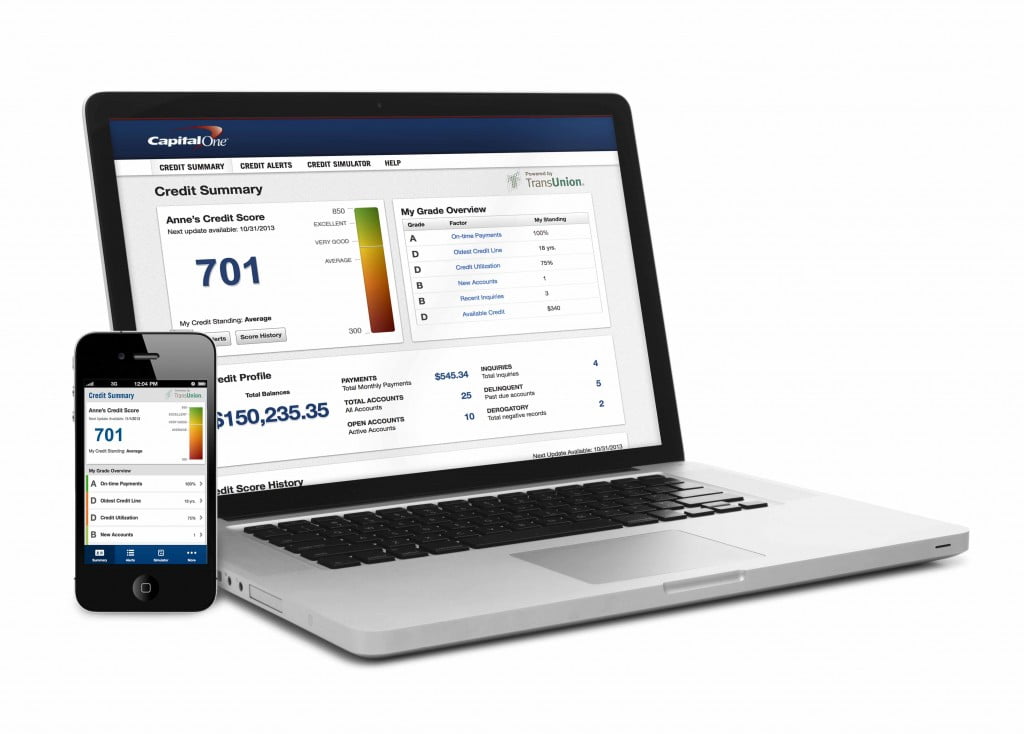

Keeping tabs on your credit score is a great way to help maintain good credit health. So people with Capital One credit cards will be happy to know that starting very soon, the bank will roll out free credit scores and a suite of credit-education tools. The new offering is called Credit Tracker, and it …

Capital One Rolls Out Credit Tracker, Free Credit Scores for Customers Read More »

Credit monitoring is an electronic, subscription-based service for consumers who want to track their credit activity at the “Big 3” U.S. credit reporting agencies — Equifax, Experian and TransUnion. Credit bureaus, credit scoring firms and other companies typically sell credit monitoring services for a fee ranging from about $10 to $20 a month. But some …

Checking your FICO credit score at least once a year is a good way to stay on top of your credit rating. That’s why you may be happy to learn that myFICO.com – the consumer website of Fair Isaac, creator of the FICO score – is offering you the opportunity to get your FICO score …

Get Your FICO Credit Score Free and Help Your Credit Rating Read More »

If someone uses your personal identifying information such as your name, address, Social Security number, and credit card numbers to steal money or create a false identity, you have been a victim of identity theft. Scam artists are becoming better and better at stealing sensitive information from credit card machines, over the Web, and even …

Most financial experts agree that routinely checking your credit reports is a smart idea. If you ask those same experts about credit monitoring services, however, you’ll likely get a lot of eye-rolling and negative comments.